Agent Banking Boosts Rural Financial Flows in Bangladesh

Bangladesh’s agent banking network is playing an increasingly important role in the country’s financial system, particularly in channeling remittances to rural households.

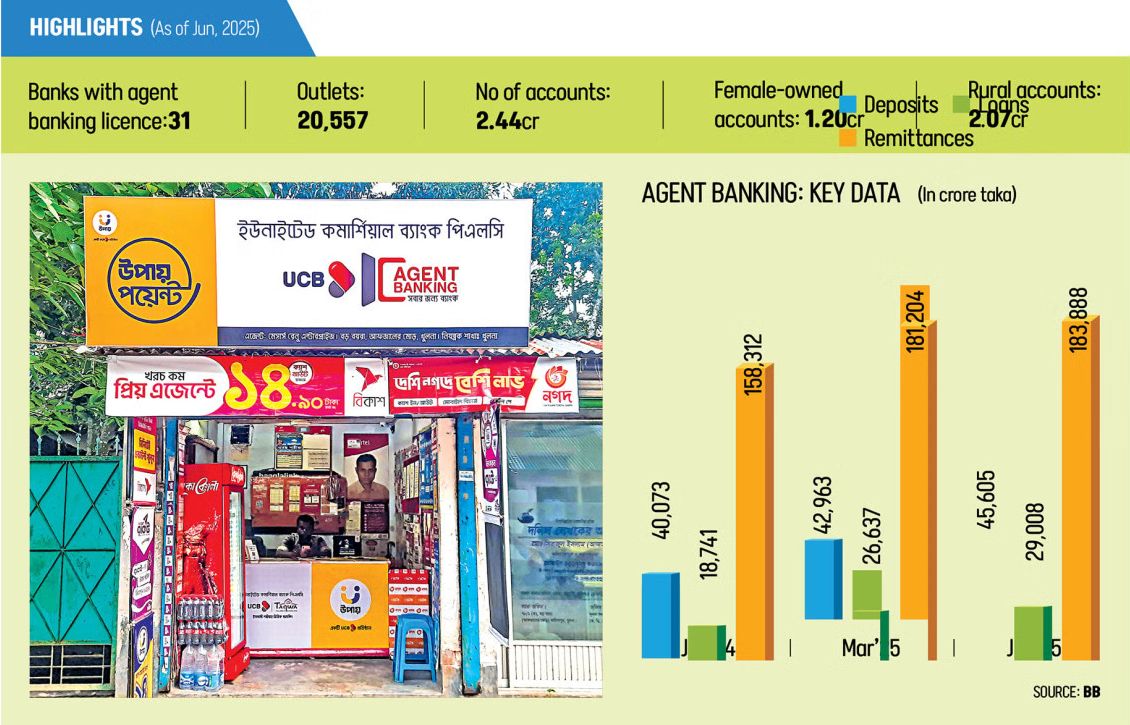

According to the latest quarterly report from Bangladesh Bank, agent banking outlets handled Tk 1,83,888 crore in remittances during the April-June period of the 2024-25 fiscal year, marking a 16.15 percent increase compared to the same period last year. Notably, around 90 percent of these funds reached recipients in rural areas.

Three banks dominate the agent-based remittance landscape, collectively accounting for more than 90 percent of total disbursements. Islami Bank led the way with Tk 1.01 lakh crore (55.08 percent of the total), followed by Dutch-Bangla Bank at nearly Tk 51,143 crore and Bank Asia with Tk 14,253 crore.

“Agent banking is no longer a pilot programme—it has become a mainstream channel for remittance distribution, bringing financial services closer to rural communities,” said Arief Hossain Khan, spokesperson for Bangladesh Bank. He added that the system is helping to extend inclusive finance while supporting secure and legal remittance flows.

Introduced in 2013, agent banking was designed to provide banking services in remote areas beyond the reach of traditional branches. Operated by local representatives using point-of-sale devices and mobile connectivity, agent outlets allow recipients to receive remittances within minutes. The model reduces reliance on informal channels, eliminates middlemen, and ensures transaction security.

For beneficiaries, the convenience is tangible. Bibi Hazra, a 60-year-old from Shamergaon village in Noakhali’s Senbagh upazila, receives remittances sent by her three sons working in Qatar, Dubai, and Oman through local agent banking outlets. “I no longer need to travel long distances or wait in long queues,” she said. Government incentives, such as a 2.5 percent cash bonus on remittances, are also disbursed through these outlets.

Experts note that agent banking is transforming rural financial inclusion. “Faster access to remittances means families can invest more quickly in education, healthcare, and small businesses,” said Anis A Khan, former chairman of the Association of Bankers, Bangladesh.

Banks have invested heavily in digital infrastructure to support agent networks, including mobile apps, biometric authentication, and secure transaction systems. Outlets typically operate as mini-branches equipped with tablets, biometric scanners, and safes. Transactions are entered into bank servers, receipts are signed, and funds are disbursed promptly, with agents earning Tk 53 per transaction.

Despite rapid growth, the sector faces challenges. While 30 banks are licensed to provide agent banking, only a few dominate remittance disbursement. The report also highlighted gender disparities, with female recipients still underrepresented in accessing loans and financial services. Additionally, the loan-to-deposit ratio in agent banking stood at 63.61 percent during the quarter, showing untapped potential for credit expansion.

As Bangladesh’s agent banking network continues to evolve, it is proving to be a critical mechanism for delivering financial services and fostering economic inclusion in the country’s most remote regions.

Publisher: Mustakim Nibir

Copyright © 2026 The Times OF Dhaka. All rights reserved.